당신은 온라인 연습 문제를 통해 Level-1-CFA-Exam CFA Level 2 시험지식에 대해 자신이 어떻게 알고 있는지 파악한 후 시험 참가 신청 여부를 결정할 수 있다.

시험을 100% 합격하고 시험 준비 시간을 35% 절약하기를 바라며 CFA Level 2 덤프 (최신 실제 시험 문제)를 사용 선택하여 현재 최신 713개의 시험 문제와 답을 포함하십시오.

/ 7

Question No : 1

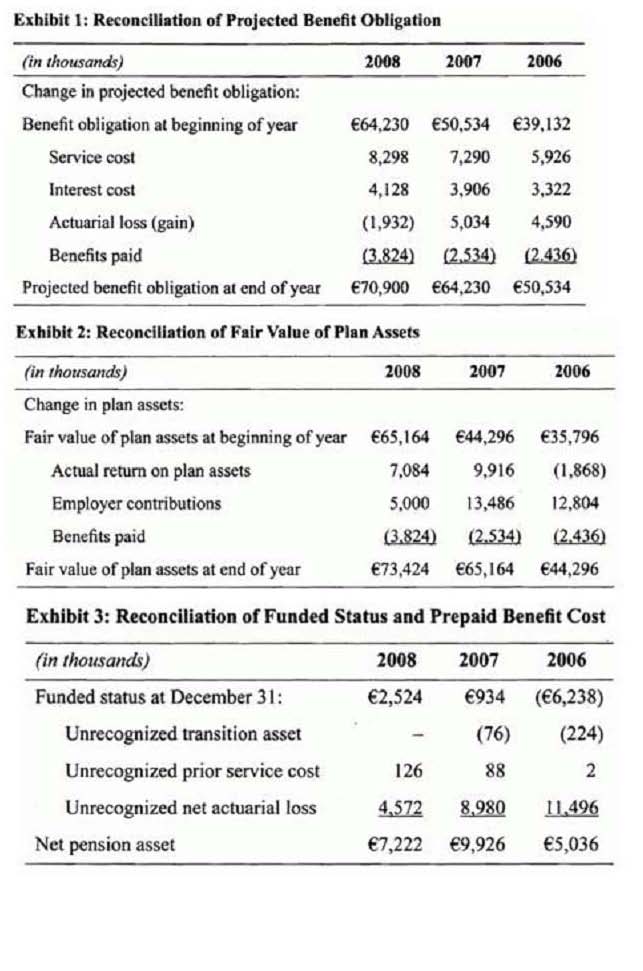

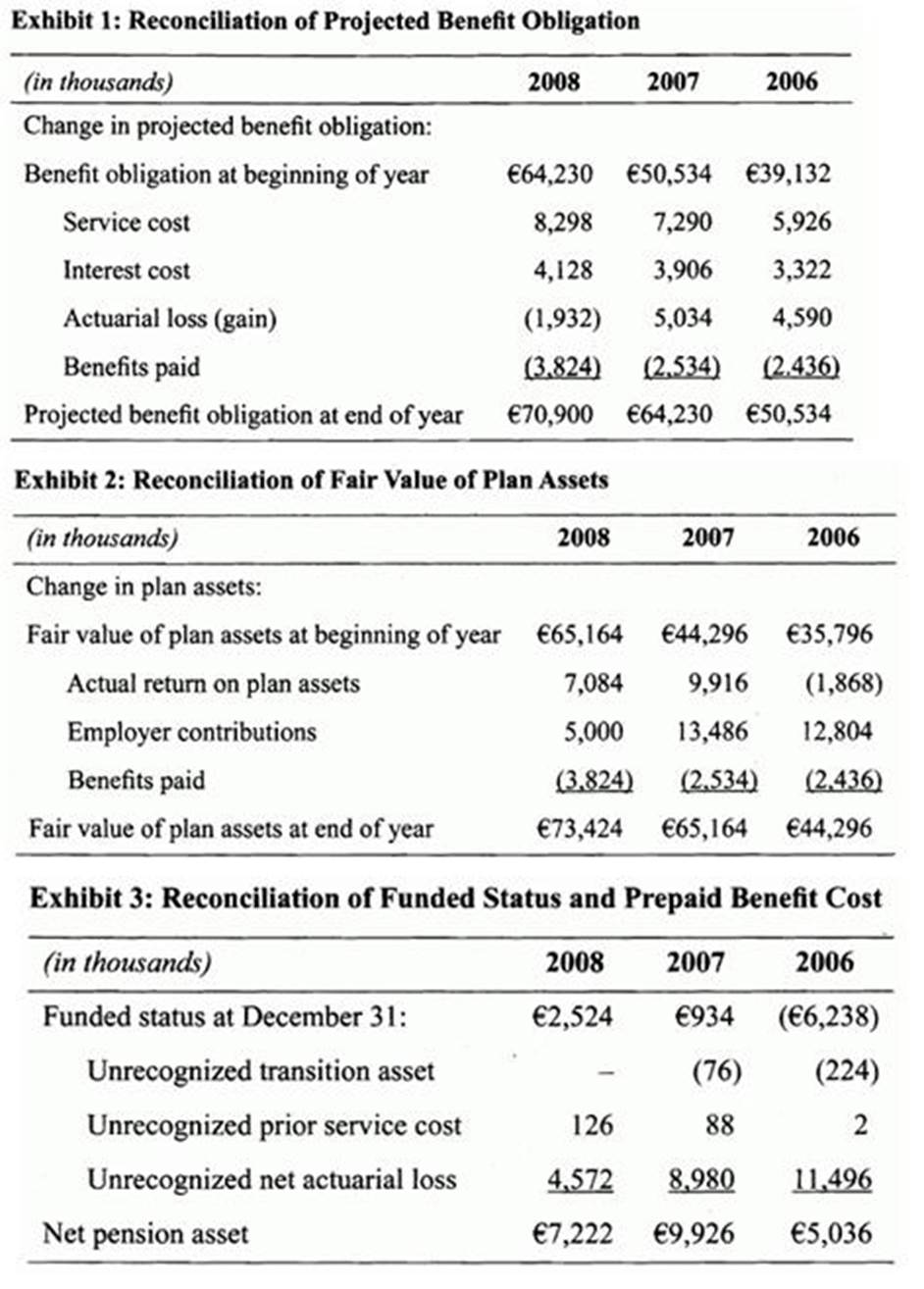

Stanley Bostwick, CFA, is a business services industry analyst with Mortonworld Financial. Currently, his attention is focused on the 2008 financial statements of Global Oilfield Supply, particularly the footnote disclosures related to the company's employee benefit plans. Bostwick would like to adjust the financial statements to reflect the actual economic status of the pension plans and analyze the effect on the reported results of changes in assumptions the company used to estimate the projected benefit obligation (PBO) and net pension cost. But first, Bostwick must familiarize himself with the differences in the accounting for defined contribution and defined benefit pension plans.

Global Oilfield's financial statements are prepared in accordance with International Financial Reporting Standards (IFRS). Excerpts from the company's annual report are shown in the following exhibits.

What was the most likely cause of the actuarial gain reported in the reconciliation of the projected benefit obligation for the year ended 2008?

정답: Explanation:

At rhe end of 2008, Global Oilfield reporred a net pension asset of 7,222 in accordance with IFRS. Under SFAS No. 158, Global Oilfields funded status of 2,524 should be reported on the balance sheet. Thus, it is necessary to reduce the net pension asset by 4,698 (7,222 as reported - 2,524 funded status). In order for the accounting equation to balance, it is also necessary to reduce equity by 4,698. (Study Session 6, LOS22.d)

Question No : 2

Stanley Bostwick, CFA, is a business services industry analyst with Morton world Financial. Currently, his attention is focused on the 2008 financial statements of Global Oilfield Supply, particularly the footnote disclosures related to the company's employee benefit plans. Bostwick would like to adjust the financial statements to reflect the actual economic status of the pension plans and analyze the effect on the reported results of changes in assumptions the company used to estimate the projected benefit obligation (PBO) and net pension cost. But first, Bostwick must familiarize himself with the differences in the accounting for defined contribution and defined benefit pension plans.

Global Oilfield's financial statements are prepared in accordance with International Financial Reporting Standards (IFRS). Excerpts from the company's annual report are shown in the following exhibits.

If Global Oilfield's retirement plan is a defined contribution arrangement, which of the following statements would be the most correct?

정답: Explanation:

In a defined contribution plan, pension expense is equal to the amount contributed by the firm. The plan participants bear the shortfall risk. There is no ABO in a defined contribution plan. (Study Session 6, LOS 22.a)

99 Stanley Bostwick, CFA, is a business services industry analyst with Morton world Financial. Currently, his attention is focused on the 2008 financial statements of Global Oilfield Supply, particularly the footnote disclosures related to the company's employee benefit plans. Bostwick would like to adjust the financial statements to reflect the actual economic status of the pension plans and analyze the effect on the reported results of changes in assumptions the company used to estimate the projected benefit obligation (PBO) and net pension cost. But first, Bostwick must familiarize himself with the differences in the accounting for defined contribution and defined benefit pension plans.

Global Oilfield's financial statements are prepared in accordance with International Financial Reporting Standards (IFRS). Excerpts from the company's annual report are shown in the following exhibits.

If Global Oilfield were to adopt U.S. pension accounting standards, what adjustment, if any, is necessary to its balance sheet at the end of 2008 assuming no taxes?

A. Decrease assets by 7,222, decrease liabilities 2,524, and decreaseequity by $4,698.

B. Decrease assets by 4,698 and decrease equity by 4,698.

C. No adjustment is necessary.

Answer: B

Explanation:

At rhe end of 2008, Global Oilfield reporred a net pension asset of 7,222 in accordance with IFRS. Under SFAS No. 158, Global Oilfields funded status of 2,524 should be reported on the balance sheet. Thus, it is necessary to reduce the net pension asset by 4,698 (7,222 as reported - 2,524 funded status). In order for the accounting equation to balance, it is also necessary to reduce equity by 4,698. (Study Session 6, LOS22.d)

Question No : 3

High Plains' average net operating assets at the end of 2008 and 2007 was $977.89 million and $642.83 million, respectively.

Which of the following statements about evaluating High Plains financial reporting quality is least accurate?

정답: Explanation:

It appears thai High Plains manipulated its earnings upward in 2008 to avoid default under its bond covenants.

However, the higher earnings are lower quality as measured by the cash flow accrual ratio. Because of the estimates involved, a lower weighting should be assigned to the accrual component of High Plains' earnings. Extreme earnings (including revenues) tend to revert to normal levels over time (mean reversion). (Study Session 7, LOS 25.b,e)

Question No : 4

High Plains' average net operating assets at the end of 2008 and 2007 was $977.89 million and $642.83 million, respectively.

Does High Plains' accounting treatment of its capital leases and receivable sale lower its earnings quality?

정답: Explanation:

A capital lease is reported on the balance sheet as an asset and as a liability. In the income statement, the leased asset is depreciated and interest expense is recognized on the liability. Thus, capitalizing a lease enhances earnings quality. An operating lease lowers earnings quality.

The receivable sale, with recourse, lowers earnings quality. The sale is treated as a collection thereby increasing operating cash flow.

However, High Plains is still responsible to the buyer in the event the receivables are not ultimately collected. Thus, the receivable sale is a collateralized borrowing arrangement that remains orT-balance-sheet. (Study Session 7, LOS 25.d,f)

Question No : 5

High Plains' average net operating assets at the end of 2008 and 2007 was $977.89 million and $642.83 million, respectively.

Using only the information found in Exhibit 1 and Exhibit 2, which of the following is most indicative of lower earnings quality?

정답: Explanation:

Maintenance and repairs, and advertising and marketing, are discretionary expenses. Both items are declining as the investment in capital assets and sales are increasing (investment in capital assets is increasing because CFI is greater than depreciation expense for the period). The change to the straight-line depreciation method is certainly less conservative.

However, measuring earnings quality based on conservative earnings is an inferior measure. (Study Session 7, LOS 25.d,f)

Note that the reason answer C is incorrect is that using LIFO as an inventory cost flow assumption during periods of stable or rising prices would cause net earnings to reflect economic (real) earnings, thereby leading to a higher quality of earnings.

Question No : 6

High Plains' average net operating assets at the end of 2008 and 2007 was $977.89 million and $642.83 million, respectively.

As compared to the year ended 2007, High Plains' cash flow accrual ratio for the year ended 2008 is:

정답: Explanation:

The cash flow accrual ratio increased during 2008 from 15% to 19%. (Study Session 7, LOS 25-d)

Question No : 7

High Plains' average net operating assets at the end of 2008 and 2007 was $977.89 million and $642.83 million, respectively.

What is the most likely effect of High Plains' revenue recognition policy on net income and inventory turnover?

정답: Explanation:

Revenue should be recognized when earned and payment is assured. High Plains is recognizing revenue as orders are received. Since High Plains still has an obligation to deliver the goods, revenue is not yet earned. By recognizing revenue too soon, net income is overstated and ending inventory is understated. Understated ending inventory would result in an overstated inventory turnover ratio. (Study Session 7, LOS

Question No : 8

High Plains' average net operating assets at the end of 2008 and 2007 was $977.89 million and $642.83 million, respectively.

Which of the following is least likely to prevent earnings manipulation?

정답: Explanation:

Bond covenants can create an incentive to engage in earnings manipulation. If High Plains remains noncompliant, the bondholders can demand immediate repayment of the debt. (Study Session 7, LOS 25.c)

Question No : 9

High Plains' average net operating assets at the end of 2008 and 2007 was $977.89 million and $642.83 million, respectively.

Which of the following is least likely to prevent earnings manipulation?

정답: Explanation:

Bond covenants can create an incentive to engage in earnings manipulation. If High Plains remains noncompliant, the bondholders can demand immediate repayment of the debt. (Study Session 7, LOS 25.c)

Question No : 10

Andrew Carson is an equity analyst employed at Lee, Vincent, and Associates, an investment research firm. In a conversation with his supervisor, Daniel Lau, Carson makes the following two statements about defined contribution plans.

Statement 1: Employers often face onerous disclosure requirements.

Statement 2: Employers often bear all the investment risk.

Carson is responsible for following Samilski Enterprises (Samilski), a publicly traded firm that produces motorcycles and other mechanical parts. It operates exclusively in the United States. At the end of its 2009 fiscal year, Samilski's employee pension plan had a projected benefit obligation (PBO) of $320 million. Also, unrecognized prior service costs were $35 million, the fair value of plan assets was $316 million, and the unrecognized actuarial gain was $21 million.

Carson believes the rate of compensation increase will be 5% as opposed to 4% in the previous year, and the discount rate will be 7% as opposed to 8% in the previous year.

This past year, Samilski began using special purpose entities (SPEs) for various reasons. In preparation for analyzing the SPE disclosures in the footnotes to the financial statements, Carson prepares a memo on SPEs. In the memo, he correctly concludes that the company will be required under new accounting rules to classify them as variable interest entities (VIE) and consolidate the entities on the balance sheet rather than report them using the equity method as in the past.

Which of the following items, when recognized, will likely increase:

PBO? Pension expense?

정답: Explanation:

An actuarial loss results from a change in actuarial assumptions. In the case of a loss, the amount of pension benefits payable in the future would increase, thus increasing the PBO. Actuarial gains have the opposite effect.

The amortization of prior service costs results in pension expense being increased gradually over a number of years, rather than all at once in the year of occurrence. In contrast, the expected return on plan assets is an "income" component in calculating pension cost (service cost and interest cost being the expense components), so recognition of expected return on plan assets would decrease pension expense. (Study Session 6, LOS 22.b)

Question No : 11

Andrew Carson is an equity analyst employed at Lee, Vincent, and Associates, an investment research firm. In a conversation with his supervisor, Daniel Lau, Carson makes the following two statements about defined contribution plans.

Statement 1: Employers often face onerous disclosure requirements.

Statement 2: Employers often bear all the investment risk.

Carson is responsible for following Samilski Enterprises (Samilski), a publicly traded firm that produces motorcycles and other mechanical parts. It operates exclusively in the United States. At the end of its 2009 fiscal year, Samilski's employee pension plan had a projected benefit obligation (PBO) of $320 million. Also, unrecognized prior service costs were $35 million, the fair value of plan assets was $316 million, and the unrecognized actuarial gain was $21 million.

Carson believes the rate of compensation increase will be 5% as opposed to 4% in the previous year, and the discount rate will be 7% as opposed to 8% in the previous year.

This past year, Samilski began using special purpose entities (SPEs) for various reasons. In preparation for analyzing the SPE disclosures in the footnotes to the financial statements, Carson prepares a memo on SPEs. In the memo, he correctly concludes that the company will be required under new accounting rules to classify them as variable interest entities (VIE) and consolidate the entities on the balance sheet rather than report them using the equity method as in the past.

What are the likely effects of the required change in accounting for SPEs on Samilski's:

Return on assets? Return on equity?

정답: Explanation:

As a result of consolidating SPEs that were previously accounted for using the equity method, assets will increase but net income and equity won't change. Therefore, return on assets will decrease, but there will be no effect on return on equity. (Study Session 5, LOS 21. c)

Question No : 12

Andrew Carson is an equity analyst employed at Lee, Vincent, and Associates, an investment research firm. In a conversation with his supervisor, Daniel Lau, Carson makes the following two statements about defined contribution plans.

Statement 1: Employers often face onerous disclosure requirements.

Statement 2: Employers often bear all the investment risk.

Carson is responsible for following Samilski Enterprises (Samilski), a publicly traded firm that produces motorcycles and other mechanical parts. It operates exclusively in the United States. At the end of its 2009 fiscal year, Samilski's employee pension plan had a projected benefit obligation (PBO) of $320 million. Also, unrecognized prior service costs were $35 million, the fair value of plan assets was $316 million, and the unrecognized actuarial gain was $21 million.

Carson believes the rate of compensation increase will be 5% as opposed to 4% in the previous year, and the discount rate will be 7% as opposed to 8% in the previous year.

This past year, Samilski began using special purpose entities (SPEs) for various reasons. In preparation for analyzing the SPE disclosures in the footnotes to the financial statements, Carson prepares a memo on SPEs. In the memo, he correctly concludes that the company will be required under new accounting rules to classify them as variable interest entities (VIE) and consolidate the entities on the balance sheet rather than report them using the equity method as in the past.

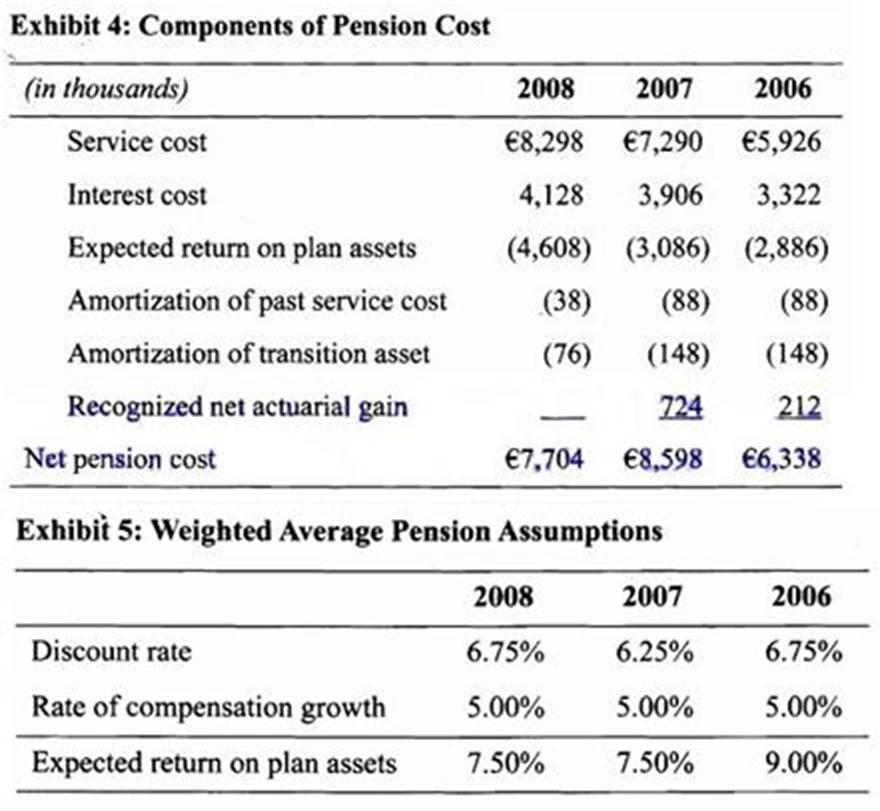

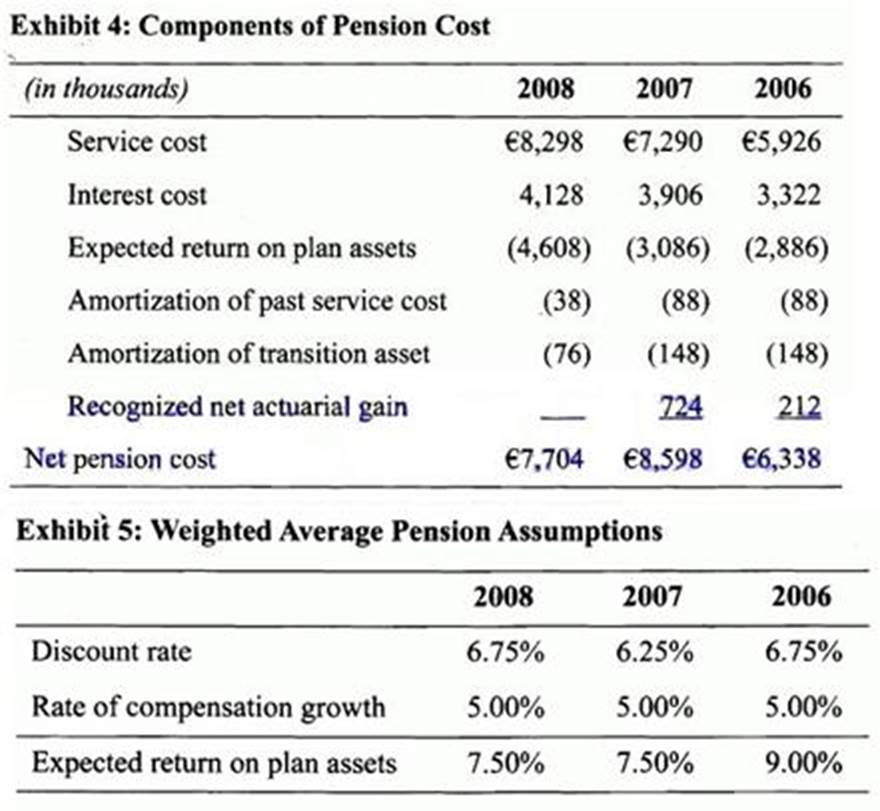

Under current U.S. GAAP pension accounting standards, the amount of the pension asset or liability that Samilski should report on its 2009 fiscal year end balance sheet is closes/ to a:

정답: Explanation:

An higher rate of compensation increase will increase the PBO. It will also increase the overall pension expense by increasing both the service and interest costs. (Study Session 6, LOS 22.b,c)

Question No : 13

Andrew Carson is an equity analyst employed at Lee, Vincent, and Associates, an investment research firm. In a conversation with his supervisor, Daniel Lau, Carson makes the following two statements about defined contribution plans.

Statement 1: Employers often face onerous disclosure requirements.

Statement 2: Employers often bear all the investment risk.

Carson is responsible for following Samilski Enterprises (Samilski), a publicly traded firm that produces motorcycles and other mechanical parts. It operates exclusively in the United States. At the end of its 2009 fiscal year, Samilski's employee pension plan had a projected benefit obligation (PBO) of $320 million. Also, unrecognized prior service costs were $35 million, the fair value of plan assets was $316 million, and the unrecognized actuarial gain was $21 million.

Carson believes the rate of compensation increase will be 5% as opposed to 4% in the previous year, and the discount rate will be 7% as opposed to 8% in the previous year.

This past year, Samilski began using special purpose entities (SPEs) for various reasons. In preparation for analyzing the SPE disclosures in the footnotes to the financial statements, Carson prepares a memo on SPEs. In the memo, he correctly concludes that the company will be required under new accounting rules to classify them as variable interest entities (VIE) and consolidate the entities on the balance sheet rather than report them using the equity method as in the past.

Based on Carson's projections of the discount rate, what are the likely effects on the projected benefit obligation (PBO) and the pension cost?

정답: Explanation:

A lower discount rate increases the PBO. It also increases the overall pension expense by increasing the service cost and, most likely, the interest cost. (For mature plans, a higher discount rate might increase interest costs. In rare cases, interest cost will increase by enough to offset the decrease in the current service cost, and pension expense will increase.) (Study Session 6, LOS 22.c)

Question No : 14

Andrew Carson is an equity analyst employed at Lee, Vincent, and Associates, an investment research firm. In a conversation with his supervisor, Daniel Lau, Carson makes the following two statements about defined contribution plans.

Statement 1: Employers often face onerous disclosure requirements.

Statement 2: Employers often bear all the investment risk.

Carson is responsible for following Samilski Enterprises (Samilski), a publicly traded firm that produces motorcycles and other mechanical parts. It operates exclusively in the United States. At the end of its 2009 fiscal year, Samilski's employee pension plan had a projected benefit obligation (PBO) of $320 million. Also, unrecognized prior service costs were $35 million, the fair value of plan assets was $316 million, and the unrecognized actuarial gain was $21 million.

Carson believes the rate of compensation increase will be 5% as opposed to 4% in the previous year, and the discount rate will be 7% as opposed to 8% in the previous year.

This past year, Samilski began using special purpose entities (SPEs) for various reasons. In preparation for analyzing the SPE disclosures in the footnotes to the financial statements, Carson prepares a memo on SPEs. In the memo, he correctly concludes that the company will be required under new accounting rules to classify them as variable interest entities (VIE) and consolidate the entities on the balance sheet rather than report them using the equity method as in the past.

Under current U.S. GAAP pension accounting standards, the amount of the pension asset or liability that Samilski should report on its 2009 fiscal year end balance sheet is closes/ to a:

정답: Explanation:

Under current U.S. GAAP pension accounting rules, which apply 10 firms with fiscal year ends after December 2006, Samilski will report the funded status of the plan on its balance sheet.

funded status = fair market value of plan assets less PBO = $316 milli on less $320 million = $4 million underfunded Therefore. Samilski will report a $4 million liability on its balance sheet. (Study Session 6, LOS 22.b)

Question No : 15

Andrew Carson is an equity analyst employed at Lee, Vincent, and Associates, an investment research firm. In a conversation with his supervisor, Daniel Lau, Carson makes the following two statements about defined contribution plans.

Statement 1: Employers often face onerous disclosure requirements.

Statement 2: Employers often bear all the investment risk.

Carson is responsible for following Samilski Enterprises (Samilski), a publicly traded firm that produces motorcycles and other mechanical parts. It operates exclusively in the United States. At the end of its 2009 fiscal year, Samilski's employee pension plan had a projected benefit obligation (PBO) of $320 million. Also, unrecognized prior service costs were $35 million, the fair value of plan assets was $316 million, and the unrecognized actuarial gain was $21 million.

Carson believes the rate of compensation increase will be 5% as opposed to 4% in the previous year, and the discount rate will be 7% as opposed to 8% in the previous year.

This past year, Samilski began using special purpose entities (SPEs) for various reasons. In preparation for analyzing the SPE disclosures in the footnotes to the financial statements, Carson prepares a memo on SPEs. In the memo, he correctly concludes that the company will be required under new accounting rules to classify them as variable interest entities (VIE) and consolidate the entities on the balance sheet rather than report them using the equity method as in the past.

Is Carson correct with respect to defined contribution plans?

정답: Explanation:

Statement 1: Employers often face onerous disclosure requirements―incorrect; the accounting is quite simple and the onerous disclosure requirements are more characteristic of defined benefit plans.

Statement 2: Employers often bear all the investment risk―incorrect; benefits received by each individual employee on retirement depends on the investment performance of each individuals personal retirement fund. Thus, the employees bear the investment risk.

Therefore, both statements arc incorrect. (Study Session 6, LOS 22.a)